As we know, automation is set to have a transformative effect on the physical retail experience. The prevalence of cashier-less retail is growing with the expansion of Amazon Go and major players like Sainsbury’s, Walmart, Alibaba, JD and now even Lenovo entering the space. And over time, consumers will likely become more and more comfortable in the “New Retail” environment that integrates online and offline customer experience (CX), but is notably lacking in one area: human interaction.

We know from history that as industries move toward automation, efficiency increases and prices fall. However, older models that are less efficient and more expensive tend to linger and transform themselves into premium-priced offerings, where “inefficiency” becomes a central element of the customer experience. Fast food, for example, was invented decades ago, but the world is still full of Casual and Fine Dining restaurants. Consumers understand that it will take longer and cost more to eat at a restaurant where the food is made to order and served to them by waitstaff. And they are willing to accept this “inefficiency” because they place value on other aspects of the dining experience.

This raises the interesting question of whether or not there is an opportunity for brands to capitalize on this connection between “inefficiency,” premium pricing and human interaction in an increasingly automated, cashier-less world.

Big Village recently ran a survey on this topic with a representative sample of 1,003 US consumers using our Online CARAVAN® omnibus. We asked consumers if they would be willing to pay a premium in order to ensure human assistance in a future scenario in which automated, cashier-less retail was more common. We asked this question in relation to a variety of common retail settings. Roughly two-thirds of consumers (64%) say they would pay a premium in at least one category. This willingness is even higher among younger-age segments, particularly those 18-34 (74%), indicating that this is a trend with some momentum.

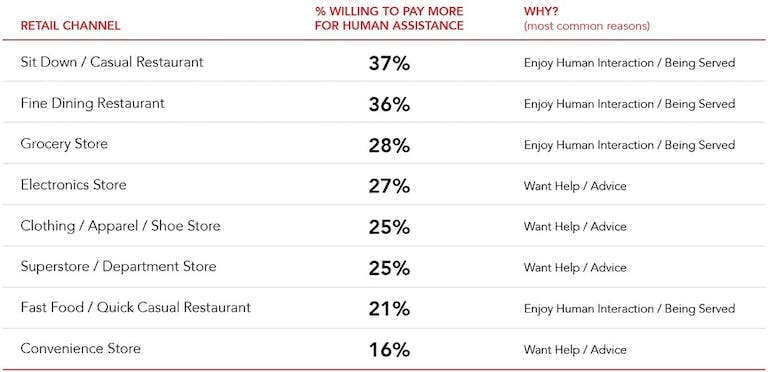

When looking at the categories individually, a quarter or more of consumers indicated they would be willing to pay a premium to ensure the availability of human assistance in their future retail experiences, with the exception of Convenience Stores. Perhaps not surprisingly, non-Fast Food restaurants received the highest ratings, with more than a third of consumers saying they would be willing to pay a premium at Casual (37%) and Fine Dining (36%) restaurants. At first glance, the restaurant industry may seem like an awkward fit for a move towards automation, but the trend is already in full swing.

Consumers most commonly attribute their willingness to pay more in food-related categories to the fact that they enjoy interacting with other people in these situations, and being served is a key element of the experience. In other channels, the desire to have someone available to answer questions and provide advice is the most common reason given.

Here is the full list of categories tested:

We then asked those who would be willing to pay more how much additional cost they would be willing to bear, with the average responses clustered just above 10% in most categories.

Finally, in order to rank the various retail channels tested in terms of total opportunity, we created an index to measure the combined effect of consumers’ willingness to pay more in a given category, along with how much more they are willing to pay. We call this the People Premium and the formula is simple: [% willing to pay more] x [average percentage of increased payment] ÷ [100] and rounded to the nearest whole number.

Here are how the various retail categories scored in terms of the People Premium index:

We are only at the dawn of the automation of physical retail and the New Retail revolution, but glimpses of human-enabled counter-trends that we call Slow Retail are emerging.

The three most important takeaways for brands from the research we conducted are:

- A significant minority of consumers in most retail channels are willing to pay a relative price premium for a human-enabled retail experience (i.e. the People Premium)

- The additional amount these consumers are willing to pay is approximately 10%

- Younger consumers (18-34) are the age group generally most open to paying this additional cost

In a future where the physical retail experience is increasingly automated and devoid of human interaction, brands have the opportunity to leverage the power of human connection to differentiate and capture value through a relative price premium.

Learn how Big Village can help increase your customer experience.