Integrating High-Touch with High-Tech in Intermediary Business Models

The ecosystems of intermediary-led business models – like wealth management and insurance – have altered from the onset of the COVID-19 pandemic. From the interactions between the provider firm to advisors and agents all the way through the end customer, the face of these relationships has evolved from highly personalized to one that relies heavily on technology – supporting operations as well as personal interactions.

To be fair, technology is not new in the world of financial services. Robo-advisors are growing by the day, digital banking is the new norm and contactless payments are a must. However, the COVID-19 pandemic has shone a light on the need for technology to keep the financial services industry buzzing, and the changes of today are here to stay.

Taking a Closer Look at the B2B Workflow

In intermediary-led business models there are many moving parts in the sales cycle. The provider company, whether it’s an asset manager, insurance firm or banking institution is tasked with tailoring solutions that appeal both to the intermediary seller (i.e. agents or advisors) as well as the end client themselves. The multiple touchpoints in this process lends to a higher emphasis on relationships in business interactions – where each party is relying on the other to get the job done.

However, these relationships have taken a back seat in recent years, as technology and the strength of solutions are increasingly important to get the job done. Recently we have seen many industries continue down a path of disintermediation, supported by technology, leading to enhanced commoditization. The trend toward higher tech reliance has already been set in motion with COVID-19 propelling it even further, seemingly overnight. And because of this many business leaders are left rethinking their entire business model and how to operate in this new world order.

Focusing on Technology to Build the New Normal

A recent Big Village survey of 146 global B2B industry experts showcased that more than half (53%) believe that accelerated use of technology will be a key mitigation strategy in the face of the COVID-19 pandemic. Technology has allowed firms to continue to conduct business, employees to interact with customers and has set the framework for new operating models. With that, it is perhaps no surprise that in the face of lockdowns and restrictions technology has become so important.

But the move to integrate technology in every fragment of our working lives is often not a seamless process. From hardware, to software, the necessary security applications and inevitable bandwidth issues, it appears as a never-ending climb to ‘master’ technology. A recent PwC survey of Financial Services executives found that 81% of banking CEOs are concerned about the speed of technological change, more than any other industry sector.1 The PwC survey was conducted pre-pandemic, underscoring how vital technology has become in maintaining operations and accelerating growth in the future. And this is a trend that is here to stay and will define future business models in the financial services space.

Assessing the Right Technological Applications…

A 2018 study by MIT, supported by insights of leading technology experts, identified seven core technologies that are set to change our world — pervasive computing, wireless mesh networks, biotechnology, 3D printing, machine learning, nanotechnology, and robotics.2 These technologies were called out as they are setting the stage for the next technological revolution and have even greater implications as they are used in combination and becoming ubiquitous in our daily lives.

For financial services leaders the workflow has, and must, change to support greater technological tools. However, key questions arise – What is the right technology mix? How should technology tools be positioned? How do we select the right partners to build the tools of tomorrow?

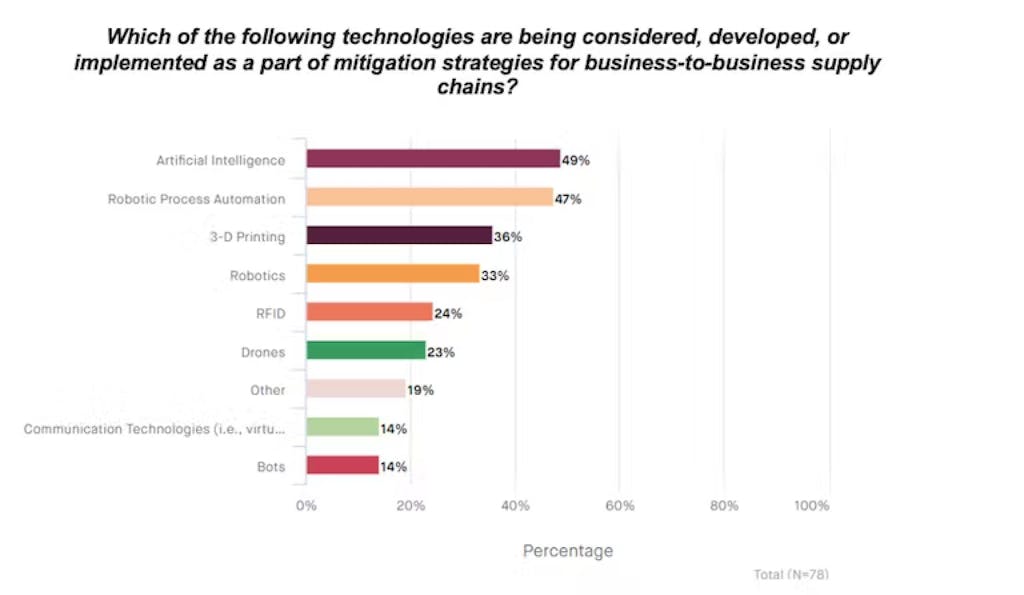

These are not simple questions for executives at any time, and especially in the face of a global pandemic. When asked what technologies are being considered, Big Village’s B2B Expert survey found that nearly half (49%) are considering the use of artificial intelligence, followed by robotic process automation (47%) and 3-D printing (36%).

… And Making it Real for Financial Services.

The broader financial services industry has remained an essential business, this means operational efficiencies are key to servicing stakeholders. The changes and business evolutions that are happening today are likely to become the new normal in the long-term.

When assessing the B2B workflow specifically, McKinsey’s recent survey of US B2B decision makers found that current sales models are here to stay. Nearly one-third (32%) of B2B decision makers noted that they are very likely to maintain current models 12+ months after the COVID-19 pandemic. 3 And we see that the sales models and client interactions of today are highly reliant on technology, downplaying the needs of face to face engagements. One of Big Village’s B2B Experts also noted that “It is astonishing how quickly technologies such as Zoom and [Microsoft] Teams (despite their flaws) have become invaluable to managing discussions and sharing information.” Though there may have been speed bumps in adjusting to the virtual environment, communication technology has allowed business to continue with minimal interruptions.

Automation, predictive technologies and video conferencing capabilities allow agents and advisors to keep conducting business as usual when in-person is a non-option. Where technology has allowed businesses to keep the lights on, there may be some level of intimacy that is lost without the presence of in-person interactions. The next phase of evolution may be replicating intimacy through technology – a process that could alter the entire customer experience in the long run.

Focusing on the Intermediary Impact

In the face of digital-only interactions, providers are being tasked with establishing cutting edge technology as a differentiator. This is increasingly important as intermediaries are always looking for the best tools and services that make their lives easier and allow them to grow their book of business in an effective and efficient manner.

Within the wealth management industry, there are some immediate marketplace examples of technological advances impacting the workflow:

- Fidelity launches digital service tools for advisors: Fidelity Institutional launched new digital service tools that make it even easier for advisors to navigate Wealthscape, its advisor technology platform, as clients increasingly leverage its digital tools. Fidelity also released new integrated learning experiences, called Smart Walkthroughs, to continue to drive digital adoption and advisor efficiency by walking users through key tasks and highlighting best practices. (Business Wire, May 2020)

- Merrill Lynch Rolls out new advisor workstation for the 2020s: Merrill Lynch Wealth Management is unveiling a major upgrade: the Client Engagement Workstation, or CEW, which helps its advisors interact with clients and manage the tasks they perform for them—everything from sending wire transfers to scheduling distributions from retirement accounts. CEW replaces Merrill’s Wealth Management Workstation, which is of the early 2000s and predates the iPhone. Although Merrill invested in upgrading it over the years, its workflow and core technology design remained largely the same. The new workstation’s design goals included ease of use, customization, and flexibility for its 22,000 users. (Barron’s, June 2020)

And Meeting the Needs of End Customers

Beyond the advances for intermediaries, technological integrations are more and more apparent for the end customer as well. AI applications are creating a game-changer for the financial services industry allowing for more personalized activities and enhanced processing capacity.

There are also key market examples supporting the end customer that are being debuted in the market today:

- Bank of America adds AI Driven Investing to Merrill Edge: Bank of America launched an “AI-driven investing experience” for self-directed clients on its Merrill Edge platform. The new offering, dubbed Dynamic Insights, is a client-facing dashboard that pulls together market data and portfolio insights driven by artificial intelligence as they relate, in real time, to a client’s holdings, accounts and current market conditions. (Financial Advisor IQ, May 2020)

- Vanguard Uses Data to Personalize Digital-Only Robo: The Digital Advisor will now consider factors such as the client’s risk tolerance, marital status, retirement savings rate and expected retirement income as investment criteria. The new features will offer clients personalized investment suggestions and advices. There are more than 300 possible glide path options which are designed to balance the risks with seeking wealth accumulation with tolerance for portfolio volatility. For example, if the algorithm determines that the client has an aggressive risk attitude, then the robo will recommend a glide path with a higher equity exposure than it would for a client who is less tolerant of risks. Vanguard also plans to add tools in June designed to help Digital Advisor clients manage emergency savings, handle debt and decide where to direct their cash. (Financial Advisor IQ, June 2020)

Making Sense of the New Normal: How Big Village Can Help

The COVID-19 pandemic has caused several businesses, and even broader industries, to completely rethink the way that they operate. Further exploration will be required for companies to define their strategies in the new post-pandemic world.

Big Village has broad experience in supporting the B2B environment. From manufacturing to CPG, to technology, healthcare and financial services, Big Village is equipped with the right experiences and approaches.

In helping to build new operations and processes amid COVID-19, Big Village has key insights solutions that support our clients’ technological evolutions:

Assessing External Forces:

- Adopting New Technology: For many firms adopting new technology means finding the right partners that truly understand their business and how to develop the precise technology that is needed. And as technological solutions become increasingly important it is imperative for businesses to accelerate new technology adoption. Analyzing partner options can be arduous and we can help to simplify the process.

- Evaluating the State of the Market: As the market evolves and new technology advances it is vital to maintain a pulse of market changes and key competitors to help identify white space opportunities or create differentiated options.

Building the Right Internal Approaches:

- Evolving Business Processes: With the monumental changes that are occurring in the world, businesses are also tasked with looking at internal process to assess the best next steps to grow in a post-pandemic world. At Big Village we understand that a system to address the ecosystem is important.

- Know the Customer

- Connect Customer Demands to Employee Needs

- Evaluate Process Changes with a Focus on Innovation

- By taking a holistic view at evolving business needs – we can help you innovate the process by learning what your key customer segments want and need.

Future Proofing your Business:

- Supporting Future Practices: We partner with clients to identify shifts across markets and industries that can be modelled to build future best practices. An eye on the future can be all the difference between staying ahead and falling behind.

Written by Amber McCullough, VP at Big Village Insights.

About B2B @ Big Village:

Big Village helps B2B organizations seeking to create sustainable growth as they proactively develop strategies to: 1) enter new markets, 2) innovate through products/services/processes and, 3) establish customer experience (CX) as a differentiator to grow existing customer relationships. Learn more about B2B @ Big Village.

About Expert Big Village:

Expert Big Village is a business-to-business service connecting business, technical and legal professionals to over 10,000 rigorously screened peer-recommended experts in over 30,000 areas of science, engineering, medicine/healthcare, regulation, and business. Learn more about Expert Big Village.