Beyond the immediate changes of today, the pandemic may alter how people manage their finances forever.

The Current State: A Focus on Managing for the Immediate

The COVID-19 pandemic can be described as sudden, tragic, and an utter upheaval of the way that we live. And at the same time, it can be viewed as a great equalizer; with essentially every American impacted to a certain degree. In this new world that we live in household savings are down, unemployment is (way) up and for those still employed income has weakened with dampened future expectations. As a result, spending has decreased across nearly all non-essential categories – creating a true ripple effect across all industries.

A recent examination of consumer perspectives through Big Village’s online CARAVAN® omnibus survey of 1,000 US adults found that nearly 7-in-10 (68%) consumers are concerned about their personal finances.[1] As a result, some of the immediate changes include cancelling vacations, delaying home renovations and ultimately eliminating big ticket purchases. Understanding the macro environment, this is perhaps not a surprise, and will likely set the stage for more conservative approaches in the long-term.

Financial Services Firms are Quick To Respond

By understanding their customers’ needs, financial services firms were able to quickly respond and offer flexible solutions during a time of need. Banks, credit card companies and insurance firms acted swiftly to extend deadlines, provide forgiveness in certain areas and even offer discounts where applicable. As early as March 9, the FDIC encouraged financial institutions to help meet the needs of those customers and members affected by COVID-19. Similarly, the National Credit Union Administration, which protects all federal (and most state) credit union deposits, is encouraging credit unions to assist affected members by allowing them to defer or skip some payments, extending payment due dates and waiving late fees and out-of-network ATM fees.[2]

Insurance companies are also keenly aware that their customers’ lives look very different than just a month ago, and many are offering automatic relief. Allstate and American Family were quick to announce relief efforts, Allstate will give most customers 15% of their monthly premium back in April and May, via a credit to their bank account, credit card or Allstate account. American Family will send auto insurance customers $50 for each vehicle on their policies.[3]

Through a deep understanding of their customers, financial services firms were able to meet some of their immediate needs of today. Post-pandemic it will become even more important to remain connected to those same customers and continue to create solutions that address their evolving needs.

From Spending to Saving: Immediate Changes Impact the Long-Term

Recessions and economic slow downs of the past have had profound impacts on the consumer psyche. A fear of the unknown abounds and thus creates a more conservative approach when planning. Downturns are also stressful and typically increase people’s desire for simplicity, impacting the way that they spend and live.

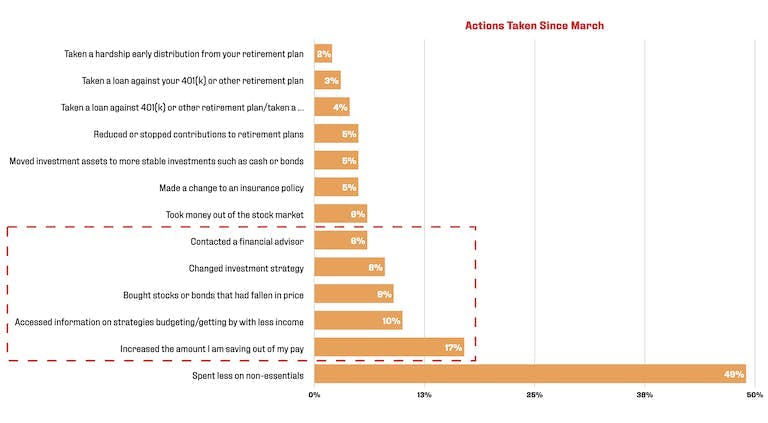

Big Village’s recent omnibus CARAVAN® study of 1,000 consumers has also shed light on how consumers may alter their financial interactions in the future. When asked “Which, if any, of the following have you done since March?” there was an indication that not all the changes have been negative, and consumers may be setting themselves up for the long game, featuring a more secure financial state post-pandemic.

We found that half of all respondents (50%) are taking a positive action that can impact their future. This includes: increased the amount that they are saving (17%), accessed information on budgeting (10%), bought stocks and bonds that have fallen in price (9%), changed investment strategy (8%) and contacted a financial advisor (6%).

If previous recessions and downturns are any indications, consumers will emerge from the COVID-19 pandemic more fiscally conservative and cautious when it comes to non-essential spending. And this can have long lasting effects and remain for years.

Creating Key Opportunities for Financial Services Firms

The air of uncertainty and concern can open the door for financial service firms to create new approaches, products and services to address the evolving needs of consumers. Many fund shops — including Charles Schwab, Fidelity and T. Rowe Price — are tweaking their financial literacy initiatives to help new and prospective investors understand the basics of investing amid market volatility. Specifically, Charles Schwab has added content to its MoneyWise platform, intended to help investors navigate the pandemic. That platform typically helps prospective investors create financial goals.[4]

Big Village’s CARAVAN® study also revealed specific areas where U.S. consumers are looking to learn more, considering the pandemic. Nearly 1-in-4 (22%) are interested in learning more about paying off debt and another 19% are interested in savings and investing strategies. Understanding the gaps in consumer knowledge can help financial service firms create a conversation with both existing customers and prospects.

Additionally, the way that consumers interact with financial firms has also seemingly changed overnight. And this change is predicated on offering highly enhanced digital tools and online services that can fully service the needs of the customer. And as customers use these tools more and more, their attitudes toward digital will change with a willingness to go online frequently and for a broader range of services. The question then becomes, how do you keep financial services customer engaged?

The result may be a closer examination of the customer journey, how they are interacting today, what are their pain points and how does that alter from the ideal state. By understanding the customer experience, whether this is a banking customer or an advisor operating in the investment space, financial services firms will be better positioned to proactively address environment changes such as the one we are in today.

Written by Amber McCullough, Vice President at Big Village Insights

[1] COVID-19: KEEPING THE PULSE OF THE CONSUMER. Big Village. April 27, 2020.

[2] List of Banks Offering Relief to Customers Affected by Coronavirus (COVID-19). Forbes. April 3, 2020.

[3] Some Insurers Offer a Break for Drivers Stuck at Home. New York Times. April 6, 2020.

[4] Shops Rework Financial Literacy Initiatives to Keep Investors Engaged. Ignites. April 27, 2020.