There has been a lot of press and discussion about the many ways that our lives have changed since the start of the pandemic as we all have created solutions to operate our lives as best we can while on lock-down. The current question, as we anticipate beginning to re-emerge from the lock-down, is which of these new behaviors will stick around.

Evolution in Financial Services Customer Experience (CX)

Now is an important time for companies to deliver the right experience for consumers as this past year has increased the focus on household finances. In this week’s Big Village Pulse study, we found that 56% of consumers agree that now is a good time to save more than they are, and 43% agree that is it a good time to invest more for retirement. Many consumers are wondering the best ways to save and invest, and turning to their banks and brokerage relationships to help them decide.

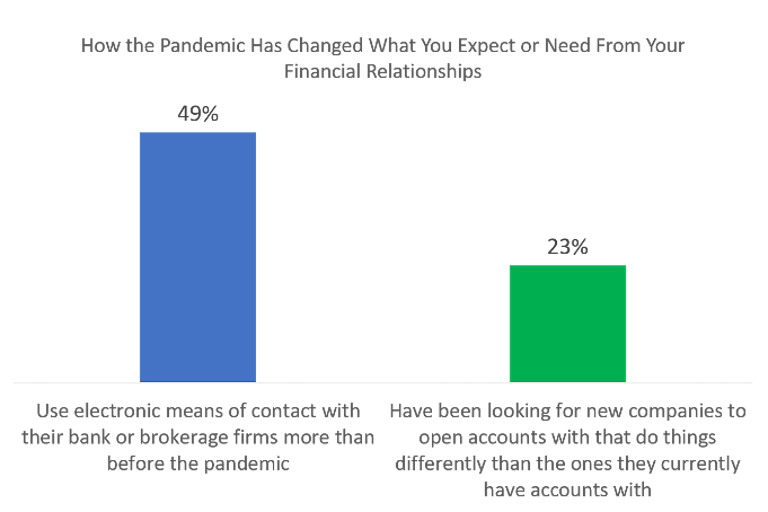

In recent years, the financial services industry has been able to pivot to electronic and remote means of doing business – many changes which had been underway before the virus emerged. Banks and investment firms have been accelerating existing digital offerings (and building new, touchless contact methods) to serve their customers during the pandemic. To their delight, and often their customers’ too, these offerings have been working well.

Adoption of mobile apps, digital tools, chat bots, curb-side services, and video consultations have proven useful for established relationships. At the same time, consumers have been exploring new relationships without some of the established, personal contact points that used to be key to engaging prospects. Just look at the explosive growth in new customers that trading platforms like Robinhood have had (even before the January GameStop explosion).

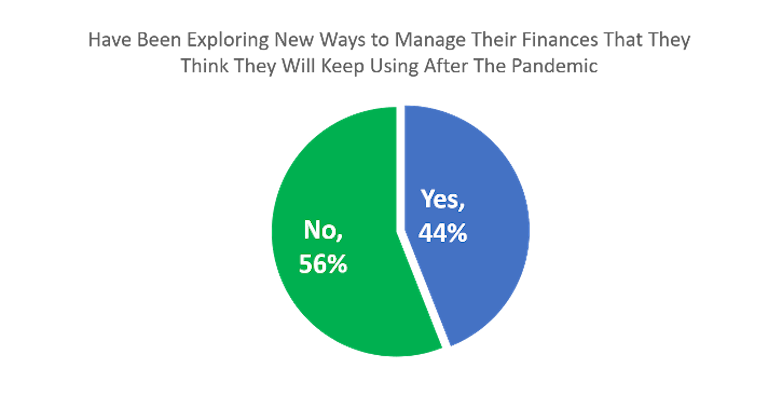

Customers have found many of these new digital or touchless interactions have been working well for them, and many are open to continuing to explore new ways.

Where Is the Future of Banking and CX Going?

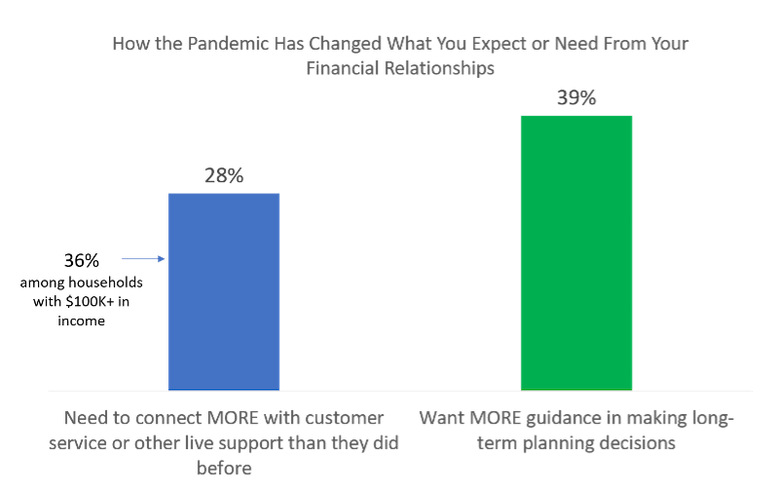

This fall, Forbes predicted that “in 2021 banking executives will misinterpret shifts in consumer behaviors and mistakenly pivot to digital-only.” It is tempting to see this adoption of scalable offerings like digital tools and imagine the potential efficiencies of a fully digital service model. However, this misses an important truth – that consumer needs from financial services have not fundamentally changed.

The acceleration of digital adoption that the pandemic has brought with it can be good news for banks and brokerage firms. It has introduced new ways to offer services that cover a larger swath of customers with scalable service models like digital tools. That being said, customers still worry about money, still need assurance, and want to trust their financial relationships to look out for them and give them the individual support they need for their unique situation. While digital tools and interactions have gained much user adoption, there is still a need to provide human interactions.

For banks and brokerage firms considering what kind of experience to deliver to their customers, finding that right balance of human-delivered, individualized consultation and digital, always-on, custom tools will be the key to both the optimal customer experience and economic service model. This is good news for financial firms’ bottom line in the long run if they can find that sweet spot where efficiencies are achieved, more customers are covered, and they are still delivering the personal touch that consumers need.

Where to Invest Your Next CX Dollar

If you are a bank with a big network of branches, a brokerage firm with a large customer service and phone-based service model, or an advisory firm with a stable of financial advisors and analysts, these resources will continue to be valuable components of your service offering. It is important to look at the digital transformation of your service that COVID-19 has accelerated as being both customer-facing and internal. Investing in the activities that make customers feel more in control and confident in their financial management AND the processes that make your human service delivery more efficiently accessible will be the most important investments now. It simply cannot be just one or the other.

Written by Margaret Rorick, SVP at Big Village Insights.